How often should we review the cash flow forecast?

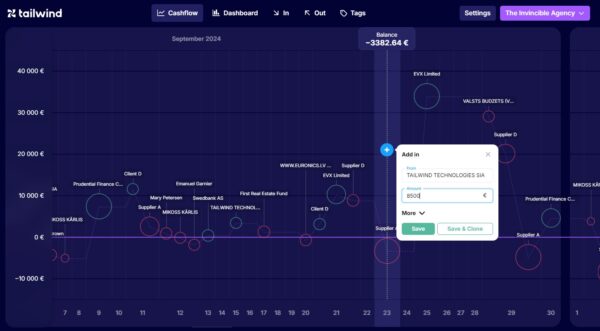

12 March 2026We have built the cash flow forecast for our company. How often should we review and update it? The best practice would be doing the reviews at least once a week. However, if the company has considerable cash reserves, less frequent reviews are also acceptable. To begin with, let’s answer another question. Why do we […]